Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

Learn, Tech & AI

If you want a completely safe way to earn fixed monthly income without worrying about market ups and downs, the Post Office Monthly Income Scheme (POMIS) remains one of the most trusted options in India.

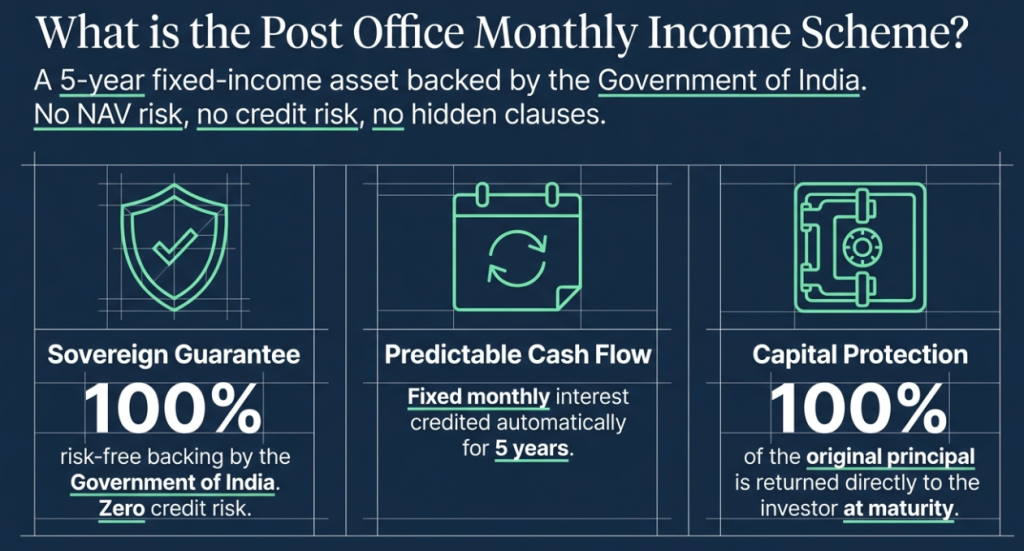

POMIS is one of India’s oldest and most dependable small savings instruments. It pays a fixed monthly interest on your deposit for five years, backed by the Government of India. No NAV risk. No credit risk. No fine print surprises buried in a 40-page insurance document.

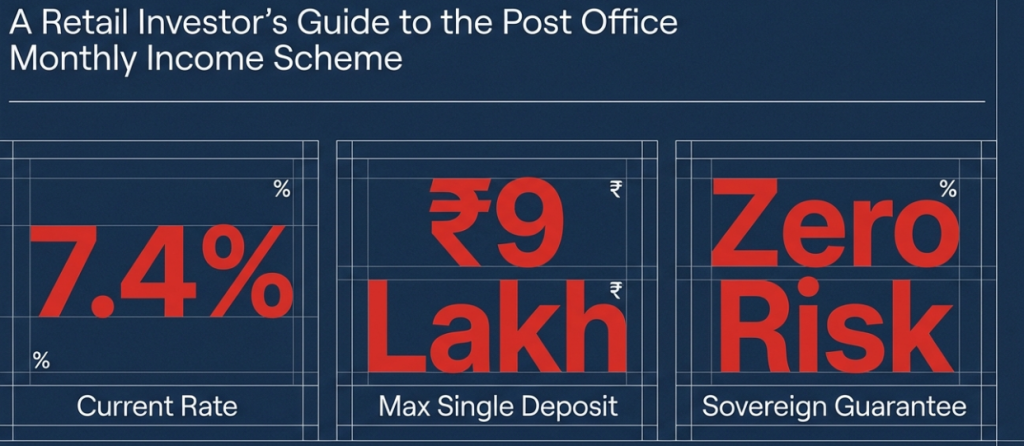

For retirees and middle-class families in places like Punjab, this scheme has long been a go-to for predictable cash flow. The current POMIS interest rate for 2026 stands at 7.4% per annum, unchanged from the previous quarter. On a maximum individual deposit of ₹9 lakh, that’s ₹5,550 per month — every month, for five years.

If you’re searching for “post office monthly income scheme”, you’re likely looking for the same thing: a zero-risk, fixed monthly payout backed by a sovereign guarantee.

This guide gives you:

✅ Current POMIS interest rate (7.4% for April-June 2026)

✅ How to calculate your exact monthly payout (with formula)

✅ Step-by-step account opening process (online + offline)

✅ Premature withdrawal penalties (and how to avoid them)

✅ POMIS vs. LIC monthly income plans (which is better?)

POMIS is a 5-year fixed-income scheme offered by India Post, designed to provide monthly interest payouts to investors. It’s 100% risk-free (backed by the Government of India) and ideal for:

The Post Office Monthly Income Scheme (POMIS) offers 7.4% per annum interest in 2026. On a maximum individual deposit of ₹9 lakh, you receive ₹5,550 per month for five years. Joint accounts allow up to ₹15 lakh, paying ₹9,250 monthly. The principal is fully returned at maturity. Interest is taxable as per your income slab.

| Feature | Details |

|---|---|

| Interest Rate | 7.4% p.a. (April-June 2026) |

| Tenure | 5 years (lock-in) |

| Minimum Deposit | ₹1,000 |

| Maximum Deposit (Individual) | ₹9 lakh |

| Maximum Deposit (Joint Account) | ₹15 lakh |

| Monthly Payout | Interest credited on the 1st of every month |

| Tax Benefit | No tax exemption (interest is taxable) |

| Premature Withdrawal | Allowed after 1 year (with penalty) |

You deposit a lump-sum amount once and receive interest every month for the next five years. At maturity you get your full principal back.

The scheme carries sovereign guarantee, which means zero credit risk. Interest is paid out directly into your linked savings account or handed over as cash, depending on the post office.

As of April–June 2026 the interest rate stands at 7.4% per annum, paid monthly. The rate has stayed unchanged for several quarters and is reviewed every three months by the Ministry of Finance.

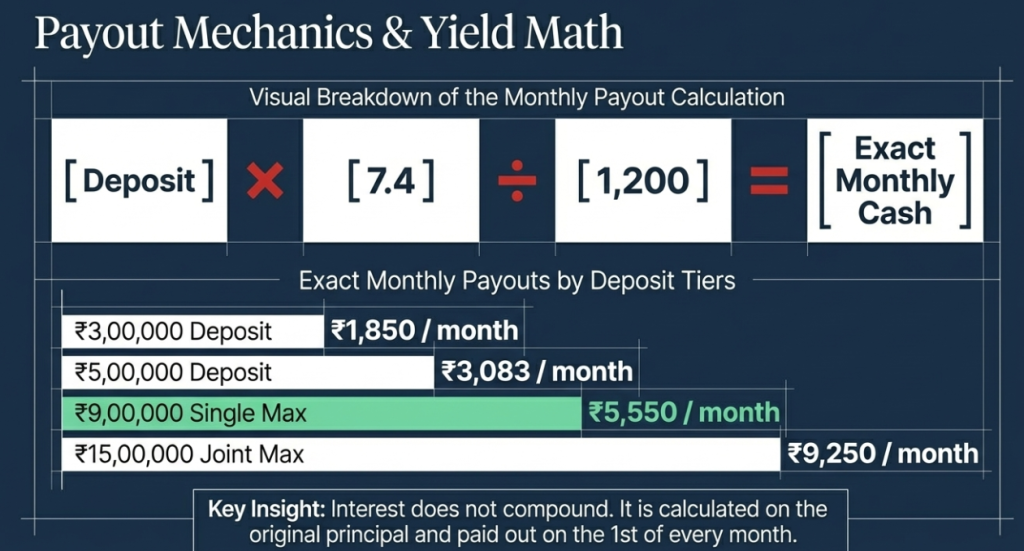

Monthly income formula (simple and exact): Monthly payout = (Principal × 7.4) ÷ 1,200

Here are real examples for the most common deposit amounts:

| Deposit Amount | Annual Interest | Monthly Income |

|---|---|---|

| ₹1,50,000 | ₹11,100 | ₹925 |

| ₹3,00,000 | ₹22,200 | ₹1,850 |

| ₹5,00,000 | ₹37,000 | ₹3,083 |

| ₹9,00,000 (max single) | ₹66,600 | ₹5,550 |

| ₹15,00,000 (max joint) | ₹1,11,000 | ₹9,250 |

These figures come straight from the official 7.4% rate. The interest is calculated on the original principal every month and does not compound inside the account.

Pro Tip:

Use the POMIS Calculator to estimate your exact payout.

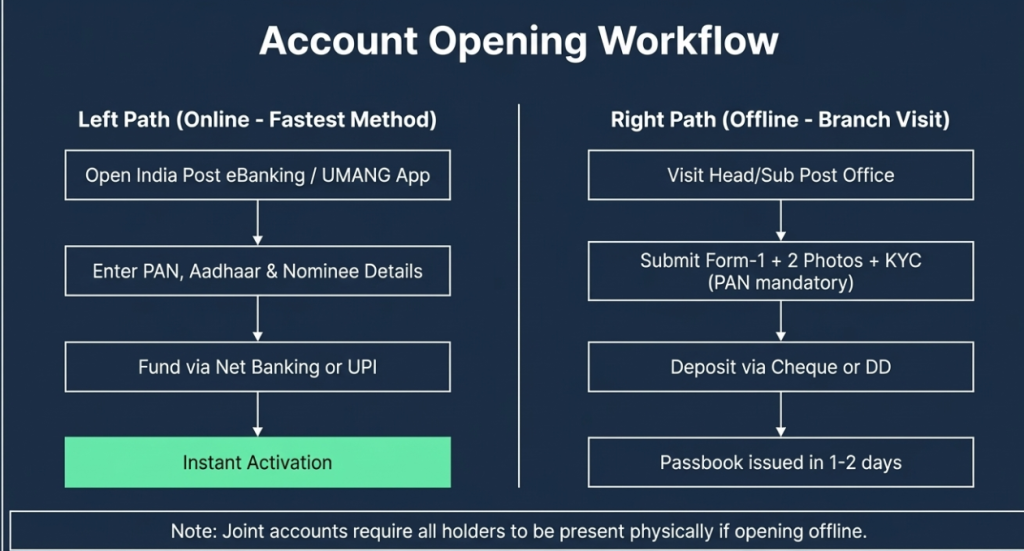

You can open a POMIS account at any Head Post Office or Sub Post Office across India. Online opening is also possible through the India Post Payments Bank (IPPB) mobile app if you already have a savings account linked.

Option 1: Online Application (Fastest Method)

Option 2: Offline Application (At Post Office)

Note:

Monthly interest is credited directly to your linked post office savings account. You can then withdraw it, transfer it, or let it accumulate — the choice is yours.

Nomination is mandatory at opening and can cover up to four nominees.

To comply with current Know Your Customer (KYC) regulations, you must physically present the original documents for verification at the post office counter alongside self-attested photocopies.

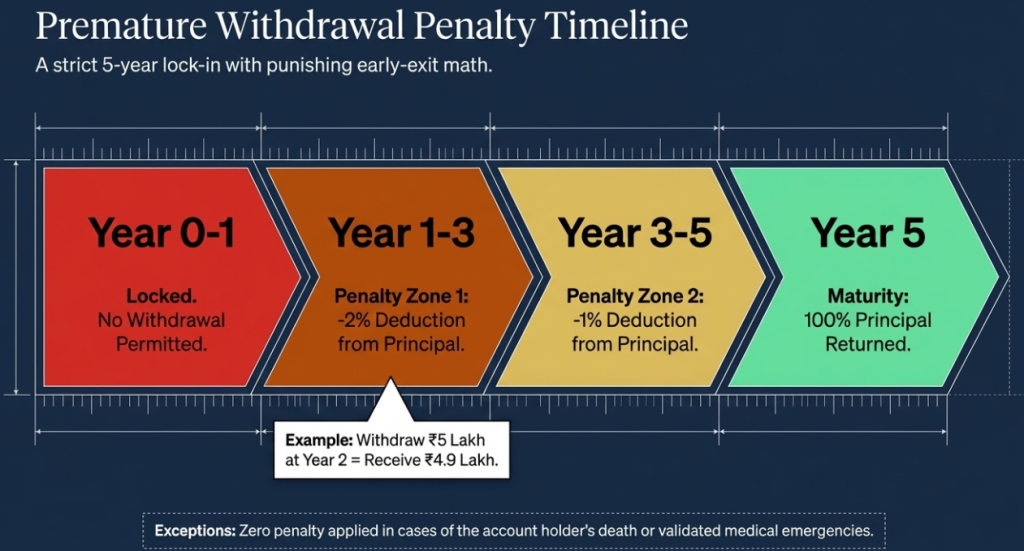

POMIS has a 5-year lock-in, but you can withdraw early after 1 year—with penalties.

| Withdrawal After | Penalty |

|---|---|

| 1 to 3 years | 2% deduction from principal |

| 3 to 5 years | 1% deduction from principal |

| After 5 years | No penalty (full amount refunded) |

Real Example:

If you withdraw ₹5 lakh after 2 years, you’ll get:

₹5,00,000 – (2% of ₹5,00,000) = ₹4,90,000

Exceptions (No Penalty):

✔ Death of account holder (nominee gets full amount)

✔ Medical emergencies (with valid proof)

We have seen many families underestimate this penalty when liquidity needs arise, so plan the five-year horizon carefully.

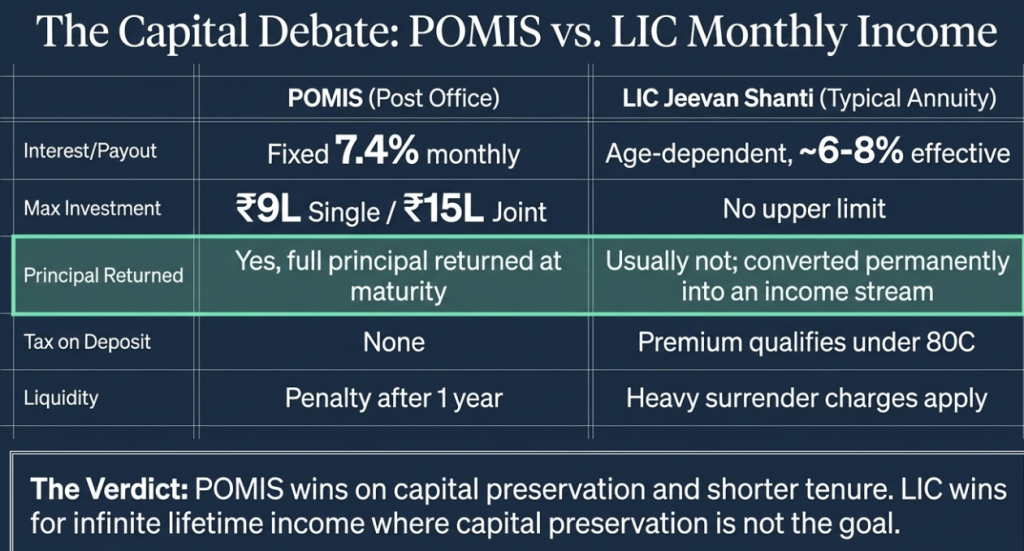

Many investors compare POMIS with LIC’s fixed income plans (specifically LIC Jeevan Akshay or LIC’s annuity products) when seeking monthly payouts. Here’s how they stack up:

| Parameter | POMIS (Post Office) | LIC Jeevan Shanti (typical annuity) |

|---|---|---|

| Interest / Payout | Fixed 7.4% monthly | Age-dependent annuity rate (usually 6–8% effective) |

| Minimum investment | ₹1,500 | ₹1.5 lakh |

| Maximum investment | ₹9L single / ₹15L joint | No upper limit |

| Principal returned | Yes, full at maturity | Usually not (pure annuity) or optional |

| Tax benefit on deposit | None | Premium qualifies under 80C |

| Risk | Sovereign guarantee | Insurance company backed |

| Liquidity | Penalty after 1 year | Surrender charges apply |

| Monthly income starts | Immediately | Can be deferred |

The key difference: LIC annuity products are designed for lifetime income — once you buy, your capital is typically gone (converted to income stream). POMIS returns your capital after 5 years, giving you flexibility to reinvest, redirect, or close the loop.

Verdict:

This is the most common misconception about POMIS.

POMIS does NOT qualify for Section 80C deduction. The deposit amount cannot be claimed as a deduction from your taxable income.

The interest earned, however, is taxable under “Income from Other Sources” at your applicable income tax slab rate. There is no TDS deducted by the post office on POMIS interest — but that does not mean the income is tax-free. You must declare it in your ITR each year.

For retirees whose total income falls below the basic exemption limit (₹3 lakh for seniors under new regime, ₹3.5 lakh for very senior citizens), the POMIS interest will effectively be tax-free — not by design, but because their overall income doesn’t cross the taxable threshold.

For higher-income individuals in the 30% slab, the effective post-tax yield at 7.4% drops to approximately 5.18%. At that point, tax-efficient alternatives like SCSS (Senior Citizen Savings Scheme) — which offers 8.2% and qualifies under 80C — may offer better net returns.

If you’re open to slightly higher risk for better returns, consider:

POMIS makes the most sense if:

It makes less sense if:

Pros of POMIS

Cons of POMIS

The Post Office Monthly Income Scheme (POMIS) is one of the safest ways to earn a fixed monthly income in India. With a 7.4% interest rate (2026), ₹9 lakh individual limit, and government backing, it’s ideal for retirees and conservative investors.

Next Steps:

For the latest small-savings rates and more retirement-income guides, bookmark TechGuruShiksha.in.

The POMIS interest rate for Q1 FY 2026-27 (April–June 2026) is 7.4% per annum. This is reviewed quarterly by the Ministry of Finance and is subject to change, though it has remained stable for several quarters.

Yes, but not before completing one year. After 1 year and before 3 years, a 2% penalty is deducted from your principal. After 3 years and before 5 years, the penalty is 1%. Interest already received monthly is not affected.

Yes. POMIS interest is taxable under “Income from Other Sources” at your applicable slab rate. No TDS is deducted by the post office, but you must report it in your ITR. It does not qualify for Section 80C deduction.

₹9 lakh for an individual account and ₹15 lakh for a joint account. A single individual can hold one individual account and also be part of a joint account, but their combined share across all accounts must not exceed ₹9 lakh.

No, POMIS is available only to Indian resident individuals. NRIs are not eligible to open a new POMIS account. Existing accounts opened before NRI status was acquired may be allowed to run to maturity subject to specific RBI guidelines.

For risk-averse investors, POMIS has the advantage of a full sovereign guarantee (versus DICGC cover of only ₹5 lakh in bank FDs). The 7.4% rate is also competitive with most public sector bank FD rates. However, bank FDs offer more flexibility in tenure and payout options.

Have a question about whether POMIS fits your current financial situation — or want us to run the numbers for a specific deposit amount? Leave a comment below and we’ll respond.

For more data-backed breakdowns of small savings schemes, fixed income instruments, and zero-risk investing strategies for the Indian market, subscribe to the TechGuruShiksha newsletter.